Consistent Monthly Income. Capital Preservation.

16+ Years Consecutive Monthly Distributions

7.30% 10-Year Annualized Total Return*

$293M Mortgages Under Administration

One fund, One focus. Delivering reliable income while preserving

capital through secured lending. Trusted by advisors since 2007.

16+ Years Consecutive Monthly Distributions

7.30% 10-Year Annualized Total Return*

$293M Mortgages Under Administration

Why Advisors Choose AP Capital

A single, focused lending strategy built around three priorities: consistent income,

capital preservation, and transparency.

Proven Performance

- 16+ yrs of consecutive monthly distributions

- 8.40% annualized return over 18 years

- No shareholder losses since inception

Conservative Underwriting

- ~57% portfolio loan-to-value (LTV)

- 716 average credit score of borrower

- 98% residential mortgages

Philosophy & Experience

- Specialist focus on residential

- Asset-first underwriting

- Management personally invested

We Lend to Homeowners

- Pooled capital is deployed into short-term mortgages secured by Canadian residential real estate

- AP Capital manages underwriting, diversification, and servicing in line with the fund’s mandate

You Receive Distributions

- Distributions are paid monthly net of fees & expenses.

- Clients can take cash or reinvest via DRIP

You Allocate

- Confirm fit within the client’s income objectives and overall risk profile

- Submit subscription documents through your dealer platform. Closings 1st and 15th of each month.

Borrowers Make Payments

- Borrowers pay scheduled interest and cash flows into the fund

- We monitor the loan book and manage renewals, prepayments, and collections as needed

You Allocate

- Confirm fit within the client’s income objectives and overall risk profile

- Submit subscription documents through your dealer platform. Closings 1st and 15th of each month.

We Lend to Homeowners

- Pooled capital is deployed into short-term mortgages secured by Canadian residential real estate

- AP Capital manages underwriting, diversification, and servicing in line with the fund’s mandate

Borrowers Make Payments

- Borrowers pay scheduled interest and cash flows into the fund

- We monitor the loan book and manage renewals, prepayments, and collections as needed

You Receive Distributions

- Distributions are paid monthly net of fees & expenses.

- Clients can take cash or reinvest via DRIP

Our Lending Process

From mortgage application to monthly distributions

A disciplined, repeatable lending process designed to protect capital and deliver steady income.

Underwriting with capital preservation prioritized

- Asset-first underwriting keeps downside protection front and center.

- Conservative LTVs and strong collateral anchor every decision.

- Independent appraisals, credit review, and legal/compliance checks support approvals.

Servicing & distributing returns

- Borrower payments are collected; performance is tracked portfolio-wide.

- Loans are actively monitored and serviced through term.

- Net income after fees and expenses is distributed monthly.

Sourcing through independent brokers

- Licensed brokers submit residential applications across Western Canada.

- Underwriting team reviews thousands of submissions every year.

- Only loans meeting standards advance to underwriting stage.

Funding short-term mortgages

- Approved loans are short-term, structured around one year.

- Pricing includes a premium versus conventional bank lending.

- That premium helps support attractive yields for shareholders.

Sourcing through independent brokers

- Licensed brokers submit residential applications across Western Canada.

- Underwriting team reviews thousands of submissions every year.

- Only loans meeting standards advance to underwriting stage.

Underwriting with capital preservation prioritized

- Asset-first underwriting keeps downside protection front and center.

- Conservative LTVs and strong collateral anchor every decision.

- Independent appraisals, credit review, and legal/compliance checks support approvals.

Funding short-term mortgages

- Approved loans are short-term, structured around one year.

- Pricing includes a premium versus conventional bank lending.

- That premium helps support attractive yields for shareholders.

Servicing & distributing returns

- Borrower payments are collected; performance is tracked portfolio-wide.

- Loans are actively monitored and serviced through term.

- Net income after fees and expenses is distributed monthly.

This repeatable approach has been central to providing reliable income and protecting investor capital throughout multiple market cycles.

Who We Lend to

AP Capital serves creditworthy borrowers who may not fit traditional bank underwriting boxes but represent attractive secured lending opportunities when viewed through an asset-first lens. The firm employs disciplined underwriting standards with a low tolerance for default risk.

Average Borrower

Credit Score

Business Owners

Established entrepreneurs with strong collateral and credit, but income that doesn't fit bank formulas

- Borrower profile: Successful owners and professionals with strong assets, solid credit, and variable year-to-year income.

- How we underwrite: We underwrite through an asset-first lens, weighing collateral strength and provable cash flow beyond standard T4 income.

- How Risk is Managed: Meaningful equity, conservative leverage, and disciplined verification help avoid assumption-based approvals.

Real Estate Investors

Experienced property investors with multiple holdings and equity. Often with portfolios banks can't assess quickly.

- Borrower profile: Multi-property owners with meaningful equity, established rental cash flow, and a proven operating track record.

- How we underwrite: We underwrite the property and the portfolio: Appraised value, rent-roll durability, borrower liquidity, and portfolio leverage.

- How Risk is Managed: Conservative LTV targets, independent appraisals, and multiple repayment/exit paths help support repayment.

Asset‑Rich Clients

Asset‑rich borrowers often have solid credit but limited traditional salaried (T4) income on paper.

- Borrower profile: Asset‑rich clients with strong credit profiles, but income that may be non‑traditional, episodic, or structure‑based.

- How we underwrite: We assess the full financial picture: collateral quality, liquidity, and a clearly defined repayment path.

- How Risk is Managed: Conservative structuring, liquidity verification, and a defined exit, keep decisions anchored to verifiable downside protection.

All mortgages go through AP Capital’s underwriting process, including independent property appraisals, borrower credit assessment, economic analysis, and compliance checks before being added to the MIC’s portfolio.

View PortfolioFund Performance & Results Share Price: $100

Portfolio

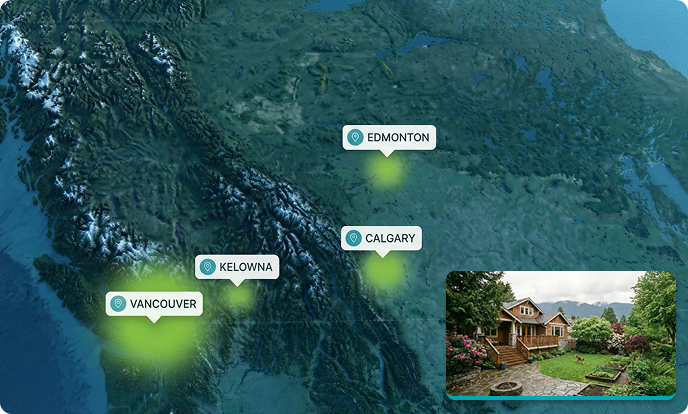

Diversified pool of short-term residential mortgages across Western Canada's key urban markets.

WHERE WE LEND

Western Canada's key urban markets.

WHAT WE LEND ON

Mainstream single-detached homes and serviced lots.

LENDING APPROACH

Short terms and conservative loan-to-value targets (target < 70%)

Advisor Resources

Everything you need to complete due diligence, implement, and communicate the strategy to clients.

Have a question? Start here. Connect with our team if you need further support.

FAQs

Key highlights:

- Single strategy MIC investment, not a mix of unrelated private credit ideas

- Conservative underwriting with an asset-first lens on residential collateral

- Repeatable process and long operating history in the same niche

- Transparent reporting and direct support for advisors

In practice, redemptions are processed on a monthly schedule, typically on the first business day of each month.

The company may implement the redemption policies outlined in the Offering Memorandum (OM), which makes liquidity subject to longer notice periods, specific conditions, and the manager’s discretion.

Investments in AP Capital MIC are best positioned as a multi-year investment, not a short-term cash substitute.

Advisors should review current liquidity terms, including both the “in practice” terms and the Offering Memorandum terms, with clients before allocating.

- Class B shares — Typically used in commission-based accounts.

- Class F shares — Typically used on fee-based advisory platforms where clients pay a separate advisory fee.

- Minimum investment — The minimum initial investment is $10,000, at a share price of $100 per share. Additional investments can be made in smaller increments.

In summary:

- Non-registered accounts — Income is reported as interest and taxed at the investor’s marginal rate.

- Registered accounts (RRSP, RRIF, TFSA, etc.) — The MIC investment can be held like many other eligible securities. Tax treatment then follows the rules of the account type.

Key talking points:

- Credit and default risk if borrowers cannot repay

- Real estate market risk if property values weaken

- Liquidity risk since the MIC investment is not exchange traded and redemptions can be limited

- Interest rate and valuation risk as rates and lending conditions change

- Manager and operational risk given the fund relies on AP Capital’s underwriting and servicing

Clients should review the full risk disclosure in the Offering Memorandum before investing.

When a loan falls behind:

- The team works with the borrower to bring payments current where possible

- If that is not successful, AP Capital enforces its security through legal remedies such as foreclosure or power of sale

- Conservative loan-to-value targets and a focus on residential property security are intended to help protect capital.

- Connect with AP Capital and share your firm and platform details

- Review the due diligence package, including Offering Memorandum, Fund Facts, and track record materials

- Complete internal approvals and selling agreements as required by your firm

- Set up the MIC investment on your platform, then schedule any training or portfolio positioning sessions for advisors